Easy one. Collect your miles if you subscribe to emails for 60 days here.

I live in a city (Los Angeles) where lots of people are independently wealthy. Unfortunately, I’m not one of these people. I do things like hustling miles to help my budget work. Most of you, as readers of this blog, are not insanely rich either. So it blows my mind how much some of you spend on annual fees. When you keep paying annual fees on a card, it kind of defeats the purpose of doing all this. And the most common reason is, “It’s so hard to keep track of all these credit cards.”

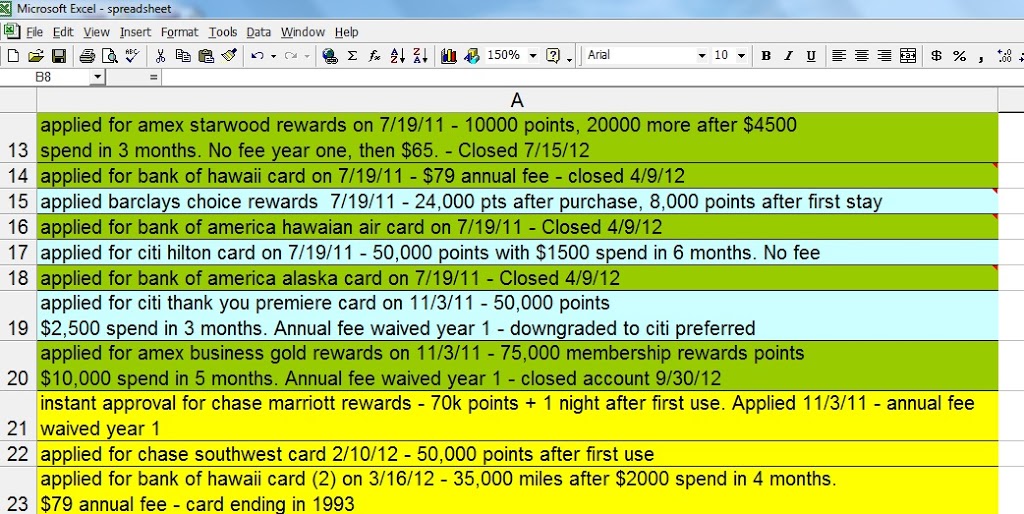

Is it really? Not for me. I spend 5 minutes a day with my spreadsheet and know exactly when an annual fee is coming. I also know when it’s time to apply for a new batch of cards. I plug in the basic information (the date I apply for a card, name of card, amount I need to spend, how fast I need to spend it, and amount of bonus miles). Then I color-code it:

Churning (verb): When you apply for a credit card you’ve already had and earn the bonus again.

(I did the same thing with the Bank of Hawaii version of the Hawaiian Airlines card)